In 2022, the economy continued to stabilize and recover from the COVID-19 pandemic but was impacted by supply-chain disruptions, rising inflation, and a tight labor market, along with a rising interest rate environment as the Federal Reserve Bank and other central banks across the globe attempted to mitigate inflationary pressures.

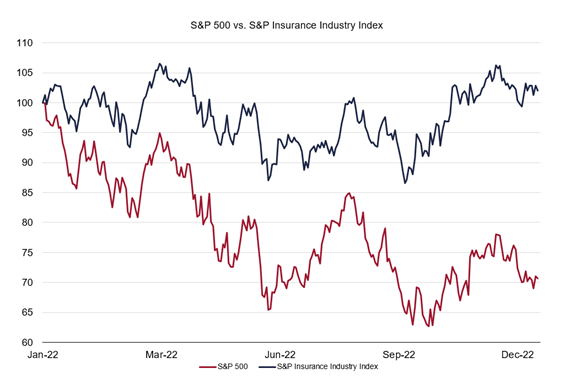

The performance of the insurance industry is generally correlated with the overall performance of the economy, as shown in the chart below; however, industry-specific factors also played an important role.

Data Provided by CapitalIQ

The insurance industry was affected by the hard market 1 in 2022, which was primarily attributable to higher interest rates, increased frequency and severity of natural catastrophes, and economic and social inflation. 2 This hard market shifted pricing power to insurers, and over the course of 2022, this tended to mitigate some of the challenges facing the broader markets during the year. As a result, in 2022, the Standard and Poor's (S&P) Insurance Industry Index (ticker INDEXSP:SPSIINS) 3 outperformed the broader S&P 500 index by 25.4 percent, with the index eking out a small gain in 2022, even while the broader markets lost significant ground during the year.

The focus of this article revolves around the key drivers in each of the subcategories in the insurance industry and how the hard market impacted these areas of the industry in 2022.

LIFE AND HEALTH INSURANCE

Although there are lingering effects of the COVID-19 pandemic, insurers are shifting away from the reactive measures used during the height of the pandemic. As both the health and economic impacts of the COVID-19 pandemic ebbed during the year, insurable events increased as individuals resumed their prepandemic lives. 4 Meanwhile, individually underwritten life insurance applications at the end of 2022 were down 5.5 percent compared to 2021 and down 2.3 percent compared to 2020, following a pandemic-induced surge. However, these percentages remained flat or showed growth in comparison to 2019 pre-COVID levels. 5

While life insurance applications were down in comparison to 2020 and 2021, this was during the peak of COVID-19 when consumer risk awareness was amplified. With the urgency of the pandemic becoming a less significant factor to the economy, the life and health insurance market is beginning to stabilize to prepandemic levels with a continued increase in demand. Furthermore, the sector continued to experience challenges, including heightened competition, technological acceleration, and regulatory shifts. 6

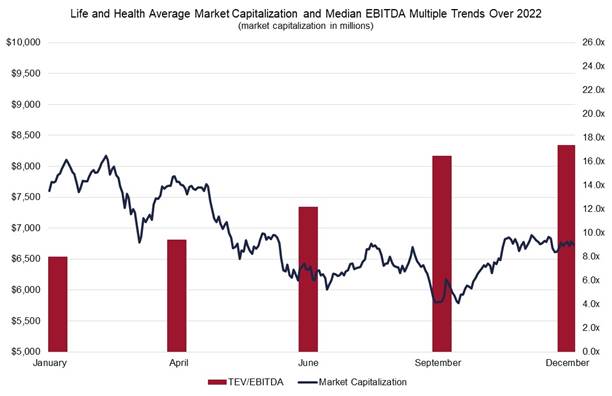

Due to the decreased demand (on a year-over-year basis) caused by the lessening effects of the COVID-19 pandemic along with the headwinds created in the overall markets, the average market capitalization of publicly traded life and health insurance companies in the United States decreased over the course of 2022; however, optimism began to appear during the fourth quarter with a rebound in valuations as shown on the chart below.

Despite the falling stock prices, valuation multiples increased steadily with enterprise value to earnings before interest, taxes, depreciation, and amortization (EBITDA) multiples increasing throughout 2022 as optimism for future growth in the sector emerged even as near-term earnings declined.

PROPERTY AND CASUALTY INSURANCE

During 2022, the insurance market stabilized for certain property and casualty (P&C) insurance lines because insurance premiums paid by end users have kept pace despite market uncertainty. However, organizations with below-average risk profiles or exposure to loss in certain states and certain industries faced inflationary pressures. Losses were lower than anticipated amid the COVID-19 pandemic and postpandemic recovery; however, P&C insurance faced inflationary pressures, supply chain disruptions, material scarcity, and labor shortages as well.

Hurricane Ian (September 23–30, 2022) affected the insurance landscape, causing many insurers to pay out billions of dollars in losses. Due to the increase in natural disasters, market conditions remained volatile for geographically challenged areas such as hurricane-prone southern coastal regions and wildfire zones on the West Coast. Hurricane Ian and Hurricane Nicole (November 7–12, 2022) contributed to global insured losses that have outpaced historical averages.

Insured property losses from natural disasters that occurred in 2022 are estimated to be between $43 billion and $72 billion. 7 Subsequently, the property insurance market expects challenges going forward as the frequency of severe natural catastrophes persists, and 2022 is expected to be the fifth consecutive year of higher premium costs. That said, growth rates are expected to be slower in comparison to 2021. Meanwhile, the casualty insurance market is approaching its fifth year of consistent rate increases for general liability and umbrella/excess liability, leading to a profitable market. 8 P&C insurance price increases were among the drivers that increased premiums in this industry. 9

Analysts focused on the P&C insurance sector remained fairly bullish throughout 2022 in regard to growth prospects as the economy remained resilient, even in light of more restrictive monetary policy during the year, and stood to benefit in comparison to 2021, which was the second most costly year recorded for insurers due to severe weather. However, alongside this growth, there were expectations for higher costs as companies would be increasing investments to manage risks arising from climate change and to propel environmental, social, and governance efforts as insurers face increasing and complicated investor scrutiny. Examples of these efforts include investments in climate sustainability, enhanced diversity in hiring, and the promotion of ethical decision-making. 10

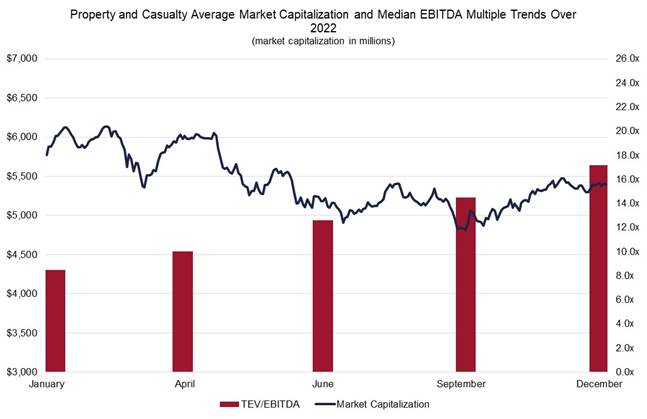

The average market capitalization of P&C firms in the United States fluctuated but maintained its value during the first 4 months of 2022 before trending downward during the next 2 months before experiencing a slight recovery during the fourth quarter. Average enterprise value to EBITDA multiples steadily increased throughout 2022, as earnings were impacted by natural disasters to a greater degree than market capitalizations, as shown in the following chart.

MULTILINE INSURERS

Due to the correlation with the life, health, and P&C markets, multiline insurers experienced similar opportunities and challenges across the insurance spectrum. International multiline insurers such as Allianz, AXA, and The Hartford generally noted an increase in revenue and profitability compared to 2021 results. 11 The Hartford reported 2022 core earnings of $2.5 billion, an increase of 13.6 percent from 2021, primarily driven by net investment income and P&C underlying underwriting gain. The Hartford's 2022 P&C lines rose 9.0 percent in 2022, driven by commercial lines premium growth of 11.0 percent during the year. 12

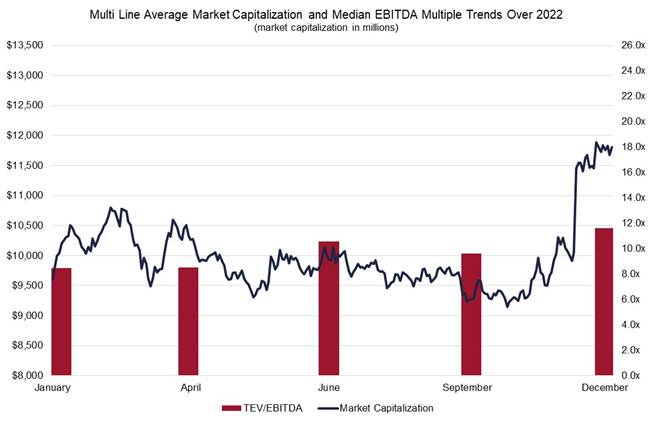

Subsequently, US-based multiline insurers saw a sharp increase in market values in the last quarter of 2022 due to better pricing, prudent underwriting, and increased exposure as more consumers became more risk averse due to the effects of the pandemic, 13 while multiples of enterprise value to EBITDA fluctuated between approximately 8.5x and 11.8x as shown in the following chart.

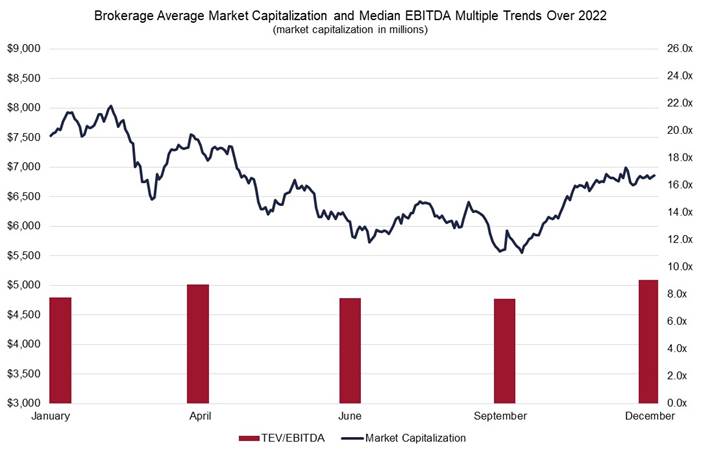

INSURANCE BROKERS

Market conditions were generally favorable for insurance brokers in 2022 benefitting from an expanded role for brokers, who are evolving to be seen more as advisers for customers, giving them insight on market changes and rate trends rather than a more transactional interaction. Due to this new trust in brokers, the market in 2022 was seen to be quite favorable after the effects of the COVID-19 pandemic subsided.

For example, Marsh and McLennan, one of the largest insurance brokerage firms in the world, reported $5.0 billion of revenue in 2022, an increase of 7.0 percent compared to 2021, and adjusted operating income growth of 13.0 percent in comparison to the previous year's results. 14 Additionally, Aon PLC reported operating income growth of 21.9 percent for the 3 months ending on September 30, 2022, compared to the prior period. 15 Given the market dynamics of 2022, the increased demand for insurance policies should allow for enhanced growth of insurance brokers in the coming years. Additionally, the introduction of artificial intelligence may allow for an enhanced level of service by brokers better matching customers' needs with their policies, further improving the outlook. 16

Although the outlook appears to be strong, throughout much of 2022, the brokerage sector average market capitalization decreased in the second quarter of 2022 due to the overall market decline driven by higher interest rates. However, the sector saw improved market performance in the fourth quarter as shown in the following chart.

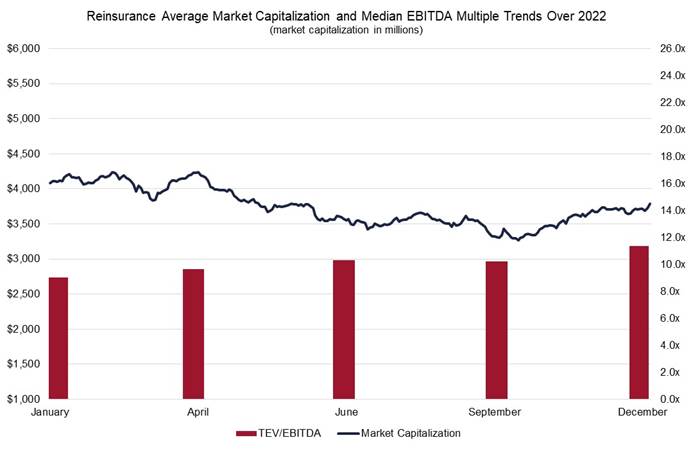

REINSURANCE

Moody's Investors Service indicated that the outlook for the global reinsurance sector is stable in comparison to 2021 as rising interest rates continue to boost investment incomes for insurers and reinsurers. 17 Moody's stated that the P&C sectors will continue to grow as a result of recent catastrophe losses, spurring demand for coverage, along with continuing inflation trends. However, dedicated reinsurance capital at year-end 2022 decreased by 8.4 percent to $435 billion from 2021.

The decline in dedicated reinsurance capital is primarily explained by the rising interest rates as it has caused asset values to deteriorate further, causing additional downward pressure on capital levels. 18 Analysts at Guy Carpenter stated that the reinsurance renewal period was delayed this year as reinsurers and cedents worked to establish a new market equilibrium. Due to this delay, insurance renewals were completed at client-issued structures and pricing. Although some reinsurers have reduced their property capacity in recent years, reinsurance companies are viewing the current market as being at an inflection point as an opportunity to increase participation as market capacity continues to stabilize. 19

Average market capitalization for the reinsurance sector was relatively flat during 2022 as the higher investment incomes in the increasing interest rate environment appeared to offset losses from natural disasters in the United States during the second half of the year. Additionally, enterprise value to EBITDA multiples for the sector also remained relatively flat, as shown in the chart below.

INSURANCE SECTOR TRANSITIONS

In 2022, there were 274 transactions globally in the insurance sector, representing a decrease compared to the 418 transactions in 2021. Merger and acquisition and public offering activity were the most significant transactions as merger and acquisition and public offering activity made up 50.7 and 48.9 percent of all transactions, respectively. 20 The United States continued to be the most active market for transaction activity in the insurance sector, with total transactions in the United States being 24.8 percent.

Acquisition activity slowed in 2022, the lowest volume the insurance sector has seen since 2019, primarily due to macroeconomic factors that were impacted by rising interest rates, higher inflation, and Russia's invasion of Ukraine. 21 One notable transaction was the acquisition of Alleghany Insurance Group by Berkshire Hathaway for $11.57 billion in October 2022. This acquisition will further expand Berkshire Hathaway's insurance operations and balance its portfolio. 22

Additionally, the second largest deal to occur in 2022 was Brown & Brown Inc.'s acquisition of Global Risk Partners Limited for $1.79 billion in March 2022 in the hopes to turn Global Risk Partners Limited into a major force in the UK retail insurance market. 23 Further, White Mountains Insurance Group, Ltd., sold its NSM Insurance Group to The Carlyle Group for $1.78 billion. 24

CONCLUSION

The market performance of the insurance industry outperformed the overall performance of the broader markets in 2022 as demand across the industry hardened, giving insurers pricing power in the inflationary environment. Market capitalizations generally have increased across the industry, indicating that companies are changing with the economic landscape. There are several factors that can affect the availability of policies that insurers can issue, including rising interest rates, increased catastrophic events, and economic/social inflation. 25 Moving forward, even as there are indications of general inflationary pressures cooling in the broader economy, there are no indications that pricing within the insurance sector will decrease, suggesting hard market conditions will continue beyond 2023. 26

Most sectors of the insurance industry continued to rebound from the impacts of the COVID-19 pandemic in 2022 in comparison to 2021, despite the overall decline in markets. In the near term, the insurance industry will be faced with opportunities and obstacles such as growing awareness of personal risk as a result of the pandemic, rising nominal rates, and technological growth. As evolution in society, technology, and the global economy continues to accelerate, companies that operate in the insurance industry will be well positioned to combat the hurdles it faced in 2022. 27

1 A hard market implies an increased demand for insurance coverage yet decreased insurance policies to supply. A hard market indicates a seller's market. During a hard market, insurers impose strict underwriting standards and are less likely to negotiate terms.

2 "2022 State of the Insurance Market," CRC Group, January 13, 2023; social inflation describes the rising costs of insurance claims above what can be explained by the overall inflation rate.

3 The index comprises stocks in the S&P Total Market Index that are classified in the GICS insurance brokers, life and health insurance, multiline insurance, P&C insurance, and reinsurance subindustries.

4 "2023 Insurance Industry Outlook," Deloitte, September 14, 2022.

5 "U.S. Life Insurance Application Activity Finishes 2022 Down versus 2021 and 2020 and Flat Compared to 2019," MIB Group Holdings, Inc., January 13, 2023.

6 "The Future of Life Insurance: Five Ways To Win," Boston Consulting Group, June 2021.

7 "2023 Commercial Property and Casualty Market Outlook," USI Insurance Services, 2023.

8 "2023 Commercial Property and Casualty Market Outlook."

9 "2023 Insurance Industry Outlook," Deloitte, September 14, 2022.

11 "The Hartford Announces Fourth Quarter and Full Year 2021 Financial Results," The Hartford, February 3, 2022; "Full Year And Quarterly Earnings Release 2022," Allianz, February 17, 2023; "Full Year 2022 Earnings—Strong Results and Continued Execution," AXA, February 23, 2023.

12 "The Hartford Announces Fourth Quarter and Full Year 2022 Financial Results," The Hartford, February 2, 2023.

13 "5 Multiline Insurers To Watch as Pandemic Impact Recedes," Yahoo, November 10, 2022.

14 "Marsh McLennan Reports Fourth Quarter and Full-Year 2022 Results," Marsh & McLennan Companies, January 26, 2023.

15 "Aon Reports Third Quarter 2022 Results," Aon PLC, October 28, 2022.

16 "Insurance Brokers Global Market Report 2022," Businesswire, June 8, 2022.

17 "Moody's—Reinsurance Sector To Benefit from Rising Prices and Strong Investment Income," Yahoo Finance, September 6, 2022.

18 "Reinsurance Capital To Drop $40 Billion at Year-End 2022: AM Best," Insurance Journal, September 5, 2022.

19 "Reinsurers at Crossroads after Difficult Jan 1 Renewals: Guy Carpenter," Reinsurance News, December 30, 2022.

20 Data obtained from the CapitalIQ database.

21 "Insurance M&A 2022 Review: Deal Activity Slows from Prior-Year Highs," S&P Global Inc., December 28, 2022.

22 "Buffett's Berkshire Hathaway Closes $11.6 billion Purchase of Alleghany Insurance Group," Associated Press, October 19, 2022.

23 "Brown & Brown Secures Acquisition of Global Risk Partners," Insurance Business America, July 6, 2022.

24 "White Mountains Completes Sale of NSM to Carlyle," Reinsurance News, August 2, 2022.

25 "2022 State of the Insurance Market," CRC Group, January 13, 2023.

26 "Hard Reinsurance Market Conditions to Continue Beyond 2023," Business Insurance, January 18, 2023.

27 "2023 Insurance Industry Outlook," Deloitte, September 14, 2022; "McKinsey Global Insurance Report 2023," McKinsey, November 16, 2022.